Additionally, CryptoKami operates on its own behalf like the US Federal Reserve (FED) by distributing and regulating the system’s KAMI Tokens based on the principle of the Compulsory Reserve Mechanism (Comreme Algorithm — CryptoKami ‘s invention) through the Regulatory Contract (CryptoKami’s invention) so financial service organizations operate based on CryptoKami platform and act as commercial banks on the system. The CryptoKami platform issues and regulates the limited 210M KAMI tokens under the Compulsory Reserve Mechanism (Comreme Algorithm) through the Regulatory Contract for various needs corresponding to its various main functions.

While all the”Blue chip” cryptocurrency such as Bitcoin, Ethereum, Litecoin, Ripple, Cardano, Stellar are focused on transaction processing, CryptoKami focuses on the automatic regulation of cryptocurrency flow in its ecosystem by the Compulsory Reserve mechanism (Comreme Algorithm) via the Regulatory ContractContract. CryptoKami’s technology and KAMI tokens will reestablish a regulated balance for the cryptocurrency market in the Wild-West industry.

1. First wave: Bitcoin and the BTC revolution

Bitcoin (BTC) is a decentralized digital currency that enables instant payments to anyone, anywhere in the world. Bitcoin uses peer-to-peer technology and operates without a central authority: transaction management and money issuance are carried out collectively by the network. The original Bitcoin software developed by Satoshi Nakamoto was released under an MIT license. Most client software, either derived or “from scratch,” also uses open source licensing. Bitcoin was the first successful implementation of a distributed crypto-currency described in part in 1998 by Wei Dai on the Cypherpunks mailing list. It is built upon the notion that money is an object or a sort of record accepted as payment for goods and services and repayment of debts in a given country or socioeconomic context. Bitcoin is designed around the idea of using cryptography to control the creation and transfer of money rather than relying on central authorities.

Bitcoins have all the desirable properties of a money-like good. They are portable, durable, divisible, recognizable, fungible, scarce, and difficult to counterfeit.

Bitcoin is P2P electronic cash that is valuable over legacy systems because of the monetary autonomy it brings to its users. Bitcoin seeks to address the root problem with conventional currency: all the trust that’s required to make it work. Justified trust is not necessarily a bad thing, but trust makes systems brittle, opaque, and costly to operate. Trust failures result in systemic collapses, trust curation creates inequality, and monopoly lock-in and naturally arising trust choke-points can be abused to deny access to due process. By using cryptographic proof, decentralized networks, and open source software, Bitcoin minimizes and replaces these trust costs.

Bitcoin Transactions:

These transactions are permissionless and borderless. The software can be installed by anyone worldwide. Bitcoins do not require any ID to use, making them suitable for people who do not have a conventional bank account or are privacy-conscious, and transactions can be made on computers by people in areas with an underdeveloped financial infrastructure.

Bitcoin transactions are also censorship-resistant, convenient, and fast. No one can block or freeze a transaction of any amount. They are irreversible once settled, like cash; however, consumer protection is still possible. Transactions are completed, or ‘broadcasted,’ in seconds and can become irreversible within an hour, are conducted online, and are available 24 hours a day, 365 days per year. Bitcoin can also be a store of value; some have said it is like having a “swiss bank account in your pocket.”

Stored Bitcoins:

Bitcoins cannot be printed or debased. Only 21 million bitcoins will ever exist.

They have no storage costs and take up no physical space regardless of amount.

Bitcoins are easy to protect and hide and can be stored and encrypted on a hard disk or paper backup. They are in a person’s direct possession with no counterparty risk. If the private key of a bitcoin is kept secret, and the transaction has enough confirmations, then no one can take them from you for any reason. Bitcoin provides the foundation for the blockchain industry and the crypto market; BTC’s market cap is currently $270 billion.

2. Second wave: Ethereum and the ETH revolution

Ethereum (ETH), like any advanced system, means different things to different people.

In a technical sense, Ethereum is a “world computer” which harks back to the days of the mainframe and is probably about as fast. Ethereum can be viewed as a single computer that the whole world can use. It notionally has only a single processor (i.e. no multi-threading or parallel execution) but has as much memory as required. Anyone can upload programs to the Ethereum World Computer, and anyone can request to execute a program that has been uploaded. This does not mean that anyone can ask any program to do anything; the program’s author can specify that requests from anyone but him- or herself be ignored, for example. Also, in a very strong sense, every program has its own permanent storage that persists between executions. Furthermore, if it is in demand, the Ethereum World Computer will always be there; it can’t be shut down or turned off.

In a more practical sense, Ethereum is an internet service platform for guaranteed computation. More than that, as a platform, it provides a set of integral features which are very useful to the developer:

user authentication via seamless integration of cryptographic signatures

fully customizable payment logic; easily create your own payment system without any reliance on third parties

100% ddos resistant up-time, guaranteed by being a fully decentralized blockchain-based platform

no-fuss storage, so developers do not need to set up secure databases; Ethereum gives you as much storage as you want

ultimate interoperability, so everything in the Ethereum ecosystem can trivially interact with everything else, from reputation to custom currencies

server free zone, so one’s whole application can be deployed on the blockchain, meaning there is no need to set up or maintain servers; let the users pay for the cost of using the service.

Ethereum creates the foundation for a new, transparent, decentralized economy base on the Ethereum blockchain. Enterprises and organizations use ETH to carry out economic transactions. ETH’s market cap is currently $70 billion.

3. Third wave: Ripple and the XRP revolution

Ripple (XRP) is a real-time gross settlement system (RTGS), currency exchange, and remittance network developed by Ripple. It is also called the Ripple Transaction Protocol (RTXP) or Ripple protocol. It is built upon a distributed open source Internet protocol, consensus ledger, and native cryptocurrency called XRP (ripples). Released in 2012, Ripple purports to enable “secure, instantly and nearly free global financial transactions of any size with no chargebacks.” It supports tokens representing a fiat currency, cryptocurrency, commodity or any other unit of value such as frequent flier miles or mobile minutes. At its core, Ripple is based around a shared, public database or ledger which uses a consensus process that allows for payments, exchanges, and remittance in a distributed process.

The network can operate without the Ripple company. Among validators are companies, internet service providers, and the Massachusetts Institute of Technology.

Used by companies such as UniCredit, UBS, and Santander, Ripple has been increasingly adopted by banks and payment networks as settlement infrastructure technology, with American Banker explaining that “from [a] banks’ perspective, distributed ledgers like the Ripple system have a number of advantages over cryptocurrencies like bitcoin,” including price and security. On 30 Dec 2017, the market capitalization of XRP was $110 billion, making it the second most valuable in the Cryptocurrency Market Cap Ranking. Ripple connects banks, payment providers, digital asset exchanges, and corporations via the RippleNet to provide one frictionless experience for sending money globally.

4. Fourth Wave: CryptoKami and the KAMI Token revolution

CryptoKami is a Decentralized Reserve System. The CryptoKami platform is like the Ethereum system, but only for third parties in the financial sector. Financial services organizations launch their ICOs and operate based on the third generation POS blockchain named CryptoKami, although its cryptocurrency is named KAMI tokens. Additionally, CryptoKami operates on its own behalf like the US Federal Reserve (FED). This is key feature and core technology of CryptoKami’s distribution and regulation of KAMI Tokens under the principle of a Compulsory Reserve Mechanism based on the Comreme Algorithm (CryptoKami’s invention) through the Regulatory Contract (CryptoKami’s invention). Therefore, CryptoKami acts as a central bank, and financial services organizations operate on CryptoKami platform like commercial banks. CryptoKami issues and regulates the total number of KAMI tokens (is limited to 210 million) under the Compulsory Reserve Mechanism based on the Comreme Algorithm through Regulatory Contract for financial third parties and end users.

For financial third parties:

Build and run “Blue-Chip”-Coins Futures Contract Exchange under the Compulsory Reserve Mechanism

Build and run a cross-chains Crypto Exchange under the Compulsory Reserve Mechanism

Build and run banking services under the Compulsory Reserve Mechanism

- Crypto deposits

- Crypto repo credit

- Cross chain payment

- Crypto-Fiat payment

For end users:

Invest in CryptoKami’s ICO under the Compulsory Reserve Mechanism

Invest in the next financial third party that launches ICOs on CrpytoKami

Trade on CryptoKami’s “Blue-Chip”-Coins Futures Contract Exchange under the Compulsory Reserve Mechanism

Trade on CryptoKami’s Cross-Chain Crypto Exchange under the Compulsory Reserve Mechanism

Staking

CryptoKami’s banking services under the Compulsory Reserve Mechanism

- Crypto deposits

- Crypto repo credit

- Cross chain payment

- Crypto-Fiat payment

The next third party Financial ICOs owners and end users as investors, holders, traders, banking services’ users must use KAMI tokens , thereby creating a massive increasing DEMAND on KAMI tokens. But the number of KAMI tokens is limited to 210 million and is regulated by the Compulsory Reserve Mechanism on every KAMI token transactions (‘flow’), so the KAMI tokens SUPPLY decreases. Therefore, according to the rule of SUPPLY and DEMAND, CryptoKami has created a strong and sustained short-, medium- and long-term SELF-GROWTH ENGINE for KAMI tokens.

While all the “Blue Chip” coins such as Bitcoin, Ethereum, Ripple, Cardano, and Stellar are focused on transaction processing, CryptoKami focuses on the automatic regulation of crypto flow in its ecosystem by the Compulsory Reserve mechanism (Comreme Algorithm) via a Regulatory Contract. CryptoKami’s technology together with KAMI tokens will reestablish a regulated balance for the crypto market in the Wild-West industry.

In May 2017, CryptoKami started developing a standalone Proof of Stake Blockchain network with a Ouroboros proof of stake algorithm (a third-generation blockchain) based on Cardano, which determines how individual nodes reach a consensus about the network. The algorithm is a crucial part of the infrastructure that supports the KAMI cryptocurrency and is a major innovation in blockchain technology. Ouroboros eliminates the need for an energy-hungry proof of work protocol, which stands as a barrier to upscaling a blockchain for much wider use.

Ouroboros is the first proof of stake protocol that has been shown mathematically to be provably secure and the first to have gone through peer review through its acceptance at Crypto 2017, the leading cryptography conference. The level of security demonstrated by Ouroboros compares to that of Bitcoin’s blockchain, which has never been compromised. Our key features and core technology are shown below:

Open-source Cardano (Ouroboros proof of stake algorithm) + compulsory reserve mechanism + Comreme Algorithm (CryptoKami’s invention) + Regulatory Contract (CryptoKami’s invention) = 3rd-generation blockchain infrastructure of CryptoKami

5. Why choose CryptoKami and KAMI Tokens?

The simple and serious answer is that the team behind CryptoKami is comprised of individuals and organizations with a wealth of experience, creativity, and financial literacy. Like the people and organizations that built up Bitcoin and Ethereum, they know and deeply understand the secrets of money, and the rule of supply and demand impacting the value of money growth behind the global economy. Therefore, they built the CryptoKami platform that provided a third-generation blockchain system and financial ecosystem and provided a staggering amount of not more than 210 million KAMI Tokens to meet third parties’ and end users’ needs. Additionally, the CryptoKami platform for third party financial services implements the ICO on it through the use of KAMI Tokens and must comply with the Compulsory Reserves Mechanism on the principle of decentralized agreements to always ensure the system’s liquidity, thereby providing strong protections for third parties and end users. The CryptoKami platform operates like the US Federal Reserve (FED) by regulating the SUPPLY and DEMAND of KAMI tokens via a Compulsory Reserve Mechanism based on the Comreme Algorithm (CryptoKami’s invention) through the Regulatory Contract (CryptoKami’s invention) for financial third parties operating on it, like the FED regulates the supply of money to commercial banks. The central bank model that regulates the SUPPLY and DEMAND of cryptocurrency is combined with financial ecosystems that have serial needs for KAMI tokens.

5.1 Regulations trigger disruption and innovation

The term RegTech has emerged to characterize innovation and emerging technology focused on solving complex regulatory challenges, enabling smarter regulation, and reducing complexity in existing regulation and compliance. There are many aspects to these activities, such as automation, data and analytics, machine learning and AI, and blockchain and cyber to name but a few. Historically, regulation was seen as a barrier to entry into Financial Services. The requirements were complex, burdensome and difficult for small, new organizations to adopt. Now we see the reverse. Many incumbents are hampered by complex processes and governance they have built up around risk and regulation, and many have also developed a significant degree of risk aversion given some of the headline-grabbing issues of the last decade. Therefore, it is surprising to find innovation influencing this area. There is a growing body of complex regulations such as Basel, Dodd-Frank, Comprehensive Capital Analysis and Review (CCAR), General Data Protection Regulation (GDPR), Markets in Financial Instruments Directive (MiFID), and the Revised Payment Service Directive (PSD2), among others, that lend themselves to solutions that can leverage technology. These regulatory hurdles can cost the world’s largest banks up to US$4 billion per annum, as many of the processes to address them are still manual. In line with this, survey respondents indicated that regulations in the digital identity authentication and anti-monetary laundering/’know your client’ (AML/KYC) spaces were strong barriers to innovation (see table below). This is due to the complex and time-consuming nature of managing detailed customer information in a global setting with constantly evolving rules and regulations. Within the DeNovo platform, we currently follow over 230 startups that help financial institutions manage their regulatory and compliance processes. These companies’ funding has increased at a CAGR of 44% over the last four years with cumulative investment at US$1.4 billion. More relevant trends include1) the automation of regulatory and compliance processes, typically utilizing AI and machine learning, and

2) increased automation of customer identification processes (e.g., KYC/AML) to reduce fraud and improve client interactions.

Regulators are also looking at ways to leverage new technology and analytics to better manage systemic risk and large amounts of data. By accumulating large amounts of data, they can analyze and assess the market and set the landscape for innovation while ensuring that they evolve. The use of blockchains is also a specific area of interest for regulators given the native ‘regulatory capabilities’ that are embedded in the technology. Transactions can be validated on the fly rather than monitored by intermediaries after the fact. We are going to see the deployment of increasingly more sophisticated technology that can monitor, capture, and analyze a broad set of data, behaviors, and activity. These are likely to ultimately provide a more comprehensive and efficient approach to regulation and risk management, although there may be some speed bumps along the way.

5.2 Regulatory barriers to innovation

In which areas do you see regulatory barriers to innovation in FinTech?Data storage, privacy and protection: 54%

Digital identity authentication: 50%

AML/KYC: 48%

New business models (crowdfunding, peer-to-peer lending) 40%

E-money/ cryptocurrency 30%

(Source: PwC Global FinTech Survey 2017)

To solve the global financial services problem, we developed the third-generation blockchain infrastructure of CryptoKami based on open source Cardano.

Open-source Cardano (Ouroboros proof of stake algorithm) + compulsory reserve mechanism + Comreme Algorithm (CryptoKami’s invention) + Regulatory Contract (CryptoKami’s invention) = 3rd-generation blockchain infrastructure of CryptoKami

Therefore, CryptoKami’s core technology combined with KAMI tokens will reestablish a regulatory balance for the crypto market in the Wild-West industry. The number of KAMI tokens is limited to 210 million and regulated by the Compulsory Reserve Mechanism on every KAMI tokens flow, so the supply of KAMI tokens SUPPLY decreases but DEMAND increases. As such, according to the rule of SUPPLY and DEMAND, CryptoKami has created a strong and sustained short-, medium- and long-term SELF-GROWTH ENGINE for KAMI tokens. This is reason you should choose the CryptoKami platform and KAMI tokens.

6. CryptoKami Platform and KAMI Token

Coin type: Standalone Blockchain TokenCoin name: KAMI token

Technology:

+ Proof of Stake Blockchain based on Cardano

+ Regulatory Contract

+ Algorithm

+ Comreme Algorithm

+ Ouroboros POS

Standard: third-generation blockchain

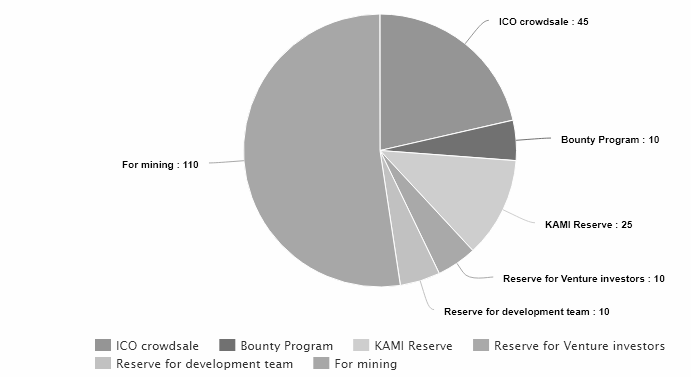

Total Controlled supply: 210,000,000 KAMI

Crowdsale Token: 45,000,000 KAMI

KAMI Tokens can be stored on:

+ PC Wallet: Window, Linux, Mac

+ E-wallet: CryptoKami.com

+ Mobile Wallet: Android app, iOS App

CryptoKami is a standalone Proof of Stake blockchain network, integrated smart contract technology, and a third-generation blockchain. KAMI (Kami Token) is a standalone Blockchain Token and an open protocol for decentralized exchanges. It is intended to serve as a basic building block that can be combined with other protocols for increasingly sophisticated control. It allows KAMI Token owners to diversify their portfolio by accessing tags related to the price of the property. KAMI Tokens allow property owners to unlock valuable assets by creating and selling or borrowing their property cards. The platform extends the liquidity and transparency of assets and reduces transaction costs. It also provides the owner of the KAMI Token detection and price diversity across multiple asset classes as it allows the creation or posting of third-party notifiers in accordance with the disclosure and management regulations and the KAMI Token contract.

KAMI Tokens Distribution (210M coins)

Learn more information here

WEBSITE: https://cryptokami.comFACEBOOK: https://www.facebook.com/cryptokamipage/

TWITTER: https://cryptokami.com

TELEGRAM: http://t.me/cryptokami

ANN: https://bitcointalk.org/index.php?topic=2855966.0

Author

Bitcointalk: https://bitcointalk.org/index.php?action=profile;u=1330327

My account’s on CryptoKami: hongquanacbd@gmail.com

Subscribe by Email

Follow Updates Articles from This Blog via Email

No Comments